Reversing the Wealth Flow: How UBI Can Empower Younger Generations

Addressing Intergenerational Economic Imbalances and Creating a Sustainable Future Through Universal Basic Income

Imagine a young couple, both working full-time jobs, struggling to save for a home, start a family, and pay off student loans. Meanwhile, their retired neighbors enjoy a comfortable lifestyle, thanks to pensions and social security benefits. This stark contrast highlights a critical issue: the current state of wealth distribution between generations. Wealth transfers from the young to the old have created economic and social imbalances that hinder the progress and potential of younger generations. However, reversing this trend through Universal Basic Income (UBI) could offer a transformative solution for society.

Understanding Wealth Transfers from Young to Old

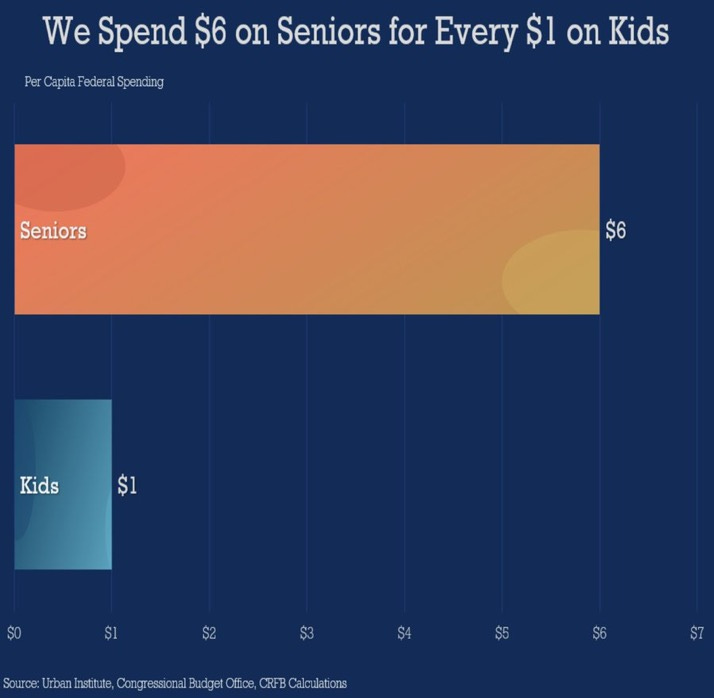

Wealth transfers from young to old refer to the economic phenomenon where resources, benefits, and financial advantages flow predominantly to older generations at the expense of younger ones. In 1998, the American population under 40 years held 13.1% of America’s total wealth. Today, those under 40 hold only 6% of the total wealth. The average baby boomer had an inflation-adjusted wealth of $140,346 in their 30s, 25% more than the wealth of millennials around the same age. This transfer can occur through various mechanisms, including social security, pensions, healthcare costs, housing costs, and debt that are disproportionately funded by the working-age population.

Historically, wealth transfers from young to old emerged as a response to societal changes, such as increased life expectancy and the establishment of social safety nets. Post-World War II policies aimed to provide financial security for the elderly, resulting in programs like Social Security in the United States. While these measures were initially beneficial, over time, they have contributed to an imbalance in wealth distribution. Current policies and practices exacerbate this wealth transfer. Social Security, for instance, is funded by payroll taxes paid by current workers to support retirees. Similarly, public pension systems and rising healthcare costs place significant financial burdens on younger generations. As the population ages, these costs continue to escalate, further straining public resources and the younger workforce.

Housing policies have significantly contributed to wealth transfers from young to old. Restrictive zoning laws and limited housing supply have driven up property values, benefiting existing homeowners and making it increasingly difficult for young people to afford their first homes. This disparity in housing affordability exacerbates the wealth gap between generations.

The accumulation of public debt is another mechanism through which wealth is transferred from young to old. Governments often borrow to fund current spending, including benefits for older generations, resulting in substantial public debt. Future generations are left to repay this debt through higher taxes or inflation, which can limit their economic opportunities and financial stability. This intergenerational burden of public debt significantly strains younger people, who must navigate the economic challenges created by previous generations’ fiscal policies.

The rising cost of education has led to substantial student loan debt for younger generations, creating a significant financial burden that older generations did not face to the same extent. Many older individuals attended college when tuition was significantly lower or even free, allowing them to enter the workforce without the heavy debt load that young people carry today. This disparity in educational costs and debt levels limits the financial mobility of younger generations, hindering their ability to save, invest, and build wealth.

The Impact of Wealth Transfers on Society

The economic impact of wealth transfers from young to old is profound. Younger generations face reduced spending power due to high taxes and limited disposable income. This situation hampers their ability to invest in education, homeownership, and entrepreneurial ventures, leading to slower economic growth and innovation. Additionally, the financial strain on public resources to support an aging population can result in increased national debt and reduced funding for other essential services.

Socially, wealth transfers create intergenerational tension and inequality. Younger people often feel burdened by the financial responsibilities imposed by older generations, leading to frustration and resentment. This dynamic can weaken social cohesion and foster a sense of injustice, as younger individuals perceive fewer opportunities and benefits compared to their elders.

A notable case study is Japan, where an aging population has placed immense pressure on younger generations. High taxes, combined with significant social security and healthcare costs, have led to economic stagnation and a declining birth rate. Young people in Japan face limited job prospects and financial insecurity, illustrating the detrimental effects of disproportionate wealth transfers.

The Case for Reversing Wealth Transfers

Reversing wealth transfers can stimulate economic growth by empowering younger generations with greater spending power. When young people have more financial resources, they can invest in education, start businesses, and purchase homes, driving economic activity and innovation. This shift can create a more dynamic and resilient economy, capable of adapting to future challenges.

Reversing wealth transfers can also improve social cohesion by addressing intergenerational inequalities. By providing younger generations with financial security and opportunities, society can foster a sense of fairness and solidarity. This approach can reduce intergenerational conflict and promote a more harmonious social environment.

Supporting younger generations is crucial for long-term economic sustainability. As the population ages, the burden on public resources will only increase. By investing in the potential of younger individuals, society can build a more sustainable and balanced economic system that benefits all age groups.

How UBI Can Help Reverse Wealth Transfers

Universal Basic Income is a policy where all citizens receive a regular, unconditional sum of money from the government, regardless of their income or employment status. UBI aims to provide financial security, reduce poverty, and promote economic stability.

UBI can redistribute wealth more equitably across generations by ensuring that younger people receive direct financial support. This income boost can alleviate the economic pressures faced by the working-age population, enabling them to invest in their futures. By increasing the disposable income of younger generations, UBI can stimulate consumer spending, drive economic growth, and reduce reliance on debt.

Socially, UBI can provide financial security and opportunities for younger people, reducing the stress and uncertainty associated with economic instability. This support can enable individuals to pursue education, career development, and entrepreneurial ventures without the constant fear of financial hardship. UBI can also enhance social mobility by providing a safety net that allows people to take risks and innovate.

Pilot programs and studies have shown the positive effects of UBI on wealth distribution. For instance, the Stockton Economic Empowerment Demonstration (SEED) in California provided monthly payments to residents and observed significant improvements in financial stability, mental health, and job prospects. Similar initiatives in Finland and other parts of the world have demonstrated that UBI can reduce poverty and enhance overall well-being.

Addressing Potential Criticisms

Critics often argue that UBI is too expensive and difficult to fund. However, there are viable funding mechanisms, such as progressive taxation, value added taxes, carbon taxes, land value taxes, and reallocating existing welfare budgets. Additionally, the economic growth stimulated by UBI can generate increased tax revenues, offsetting some of the costs.

Some opponents claim that UBI disincentivizes work and promotes laziness. However, evidence suggests that UBI can encourage entrepreneurship and education by providing a financial cushion. Moreover, the ethical argument for UBI is rooted in the principle of ensuring basic economic security and dignity for all citizens, which can lead to a more just and equitable society.

Implementing UBI presents practical challenges, including determining the appropriate amount and managing the transition from existing welfare systems. These challenges can be addressed through gradual implementation, pilot programs, and continuous evaluation to refine the policy.

Conclusion

In summary, wealth transfers from young to old create significant economic and social challenges, including reduced spending power, intergenerational tension, and financial strain on public resources. Reversing this trend through Universal Basic Income offers a promising solution by redistributing wealth more equitably, stimulating economic growth, and promoting social cohesion.

As we consider the future of our society, it is crucial to support policies that empower younger generations and create a more balanced economic system. Universal Basic Income can play a vital role in achieving these goals, fostering a more just and prosperous society for all.

Imagine a world where every young person has the financial security and opportunities to pursue their dreams without the looming shadow of economic instability. By reversing wealth transfers and embracing UBI, we can create a brighter future for future generations.

If the goal is to assist young families that are just starting out, I think that there are much more cost-effective than UBI. After all, the vast majority of the UBI will not go to young families.

I think that I have a better option:

https://frompovertytoprogress.substack.com/p/the-case-for-a-working-family-tax

Jon, nice piece about merits of UBI as a means to “reverse” the flow of benefits that currently flow from the young to the old.

At Risk & Progress, I have frequently opined that one of the greatest challenges of the 21st Century is paying for these welfare systems, which I hold are unsustainable. To make UBI affordable, if it ever can be, we are going to need to rethink these welfare programs first.

I would also caution about paying for UBI out of income taxes. My preference would be to distribute it from a social wealth fund, funded by the gifts of nature and society.